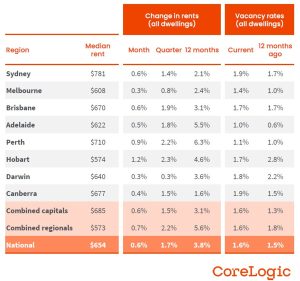

Australia’s rental market has entered another year of elevated pressure, with national rents rising 1.7% over the March 2025 quarter, according to Cotality (formerly CoreLogic). This is a sharp jump from the 0.4% quarterly increase seen in the three months to December.

But while this seasonal lift has given the impression of renewed momentum, it may be masking a broader slowdown in rental growth. In fact, while rent increases are still well above the pre-Covid average, they remain below last year’s levels – and are expected to continue moderating.

A tight market with fewer options

There are signs that rent growth is easing, but the market remains tight. Rental vacancy rates fell from 2.0% in December to just 1.6% in March – well below the 2% to 3% range considered balanced.

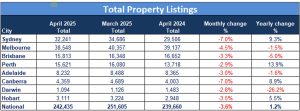

Advertised rental listings also remain significantly below historical averages, limiting choice for tenants and increasing competition. Data from SQM Research shows that total listings declined by 3.6% monthly in April; new property listings recorded a decline of 11.6%.

Meanwhile, Cotality’s Quarterly Rental Report for the March 2025 quarter reveals that unit rents are climbing faster than house rents, particularly in capital cities where demand has rebounded sharply.

Why the rental crisis isn’t going away

The pace of rent growth may be moderating, but there’s little sign that the rental crisis is coming to an end. According to SQM Research managing director Louis Christopher, the rental market remains tight, with no capital city in a balanced range.

“The combination of strong underlying growth in rental dwelling accommodation driven by ongoing surges in immigration, plus, the lack of a material increase in available rental dwellings, has kept the country in a very difficult socio-economic situation.”

Post-Covid immigration continues to fuel population growth, while new housing supply struggles to keep up. Construction activity remains constrained by high costs, labour shortages and slow approval processes.

At the same time, a study released by the Australian Housing and Urban Research Institute reveals that many investors have exited the market in recent years due to rising interest rates and policy uncertainty – shrinking the rental pool even further.

PropTrack senior economist Anne Flaherty said this imbalance was driving a new growth cycle.

“We are absolutely at the beginning of a new growth cycle…how quickly affordability deteriorates will depend on how fast the population continues to grow, and how quickly we can build new housing to keep up with that demand.”

What this means for property investors

For seasoned investors, the outlook presents both challenges and opportunities.

The good news is that rental yields are on the rise in many markets, particularly for units. Cotality research found that national gross rental yields increased five basis points over the March quarter to 3.74% – the highest since October 2019.

Yields lifted across most capitals, with Perth, Hobart and Brisbane recording the strongest gains. Sydney yields also rose slightly, up four basis points to 3.08%.

Still, national yields remain low relative to both holding costs and the pre-Covid decade average of 4.18%. Investors should also be prepared for further moderation in rental growth, particularly if affordability constraints start to bite harder.

That said, the underlying mismatch between population growth and housing supply is unlikely to resolve quickly. Over the long term, this should help support rental income stability, especially for investors who hold well-located properties in tightly held suburbs. These homes are not only more likely to attract strong rental demand, but also quality tenants willing to pay a premium.

Whether you’re expanding your holdings or simply want to structure your loans more efficiently, Clever Finance Solutions can help you make smarter finance decisions. Book a call with us to discuss your goals and needs.